Financing your new home

Getting Qualified

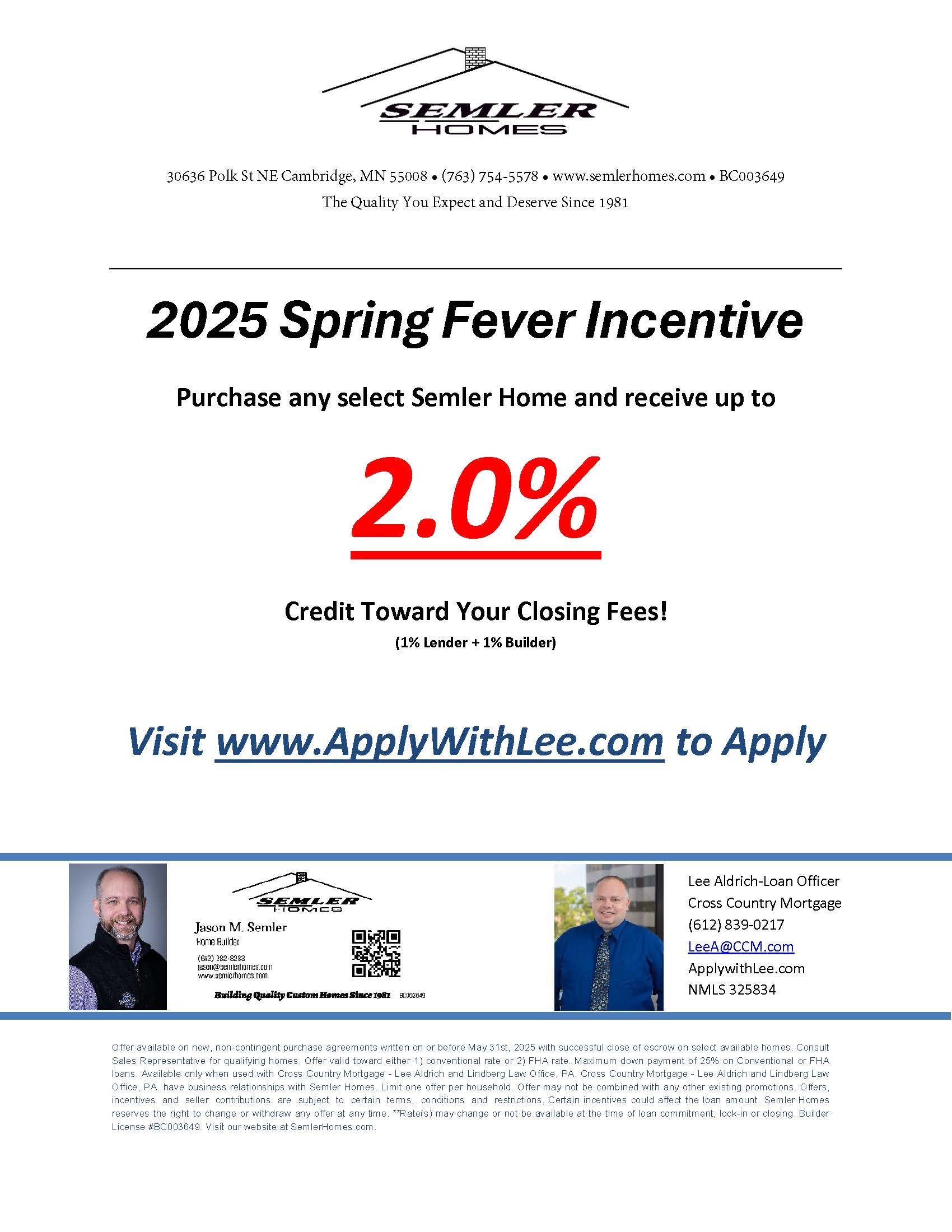

If you’re purchasing your new home using financing, the first step is being pre-qualified by a reputable lender. If you have not already been pre-qualified, please contact our preferred local loan professional below. We accept cash, conventional, FHA or VA financing.

Aldrich Lending Team

Lee Aldrich

CrossCountry Mortgage, LLC.

NMLS#:325834

612-839-0217

leea@ccm.com

www.applywithLee.com

One Time Close Construction Loan

First Time Home Buyers Assitance

Income Limited Programs

Financing FAQs

How do property taxes work on New Construction in MN?

In MN taxation values are normally set by the county assessor at the end of the year for the year after the next year. (example a November 2018 valuation assessment will become effective for tax year 2020) What this means to a New Construction Buyer in MN is if you purchase a home the same year it is completed your taxes will likely be lower for the next year so plan your budget accordingly for the increase the following year.

When is my first payment?

Typically interest is collected for the remainder of the month you close and the following month’s interest is due as part of your first payment the month after that. (example a June 10th Closing normally has a first payment due date of August 1st)

Do I need a construction loan?

For many new construction purchases the Builder will handle the financing of the construction project and the buyer will just need to have end loan approval to purchase the home from the Builder. In some cases the Builder may request that the Buyer obtain their own construction loan but most of the time this is not required.

How do I get pre-approved?

This can be done either over the phone with the Lee Aldrich Team at 612-839-0217 or via a secure online application at www.ApplywithLee.com

What is the difference between pre-approved and pre-qualified?

When a homebuyer is pre-qualified, he or she has provided the lender with the basic information to determine which loan program the homebuyer may qualify for. Whereas, when a homebuyer is pre-approved, the lender has collected, verified and presented the information needed for underwriting and approval.

What is the difference between interest rate and APR?

Your interest rate is the monthly cost you pay on the unpaid balance of your home loan. An Annual Percentage Rate (APR) includes both your interest rate and any additional cost or prepaid finance charges such as the origination fee, points, private mortgage insurance, underwriting and processing fees (your actual fees may not include all of these items). While your interest rate is the rate at which you will make your monthly mortgage payments, the APR is a universal measurement that can assist you in comparing the cost of mortgage loans offered by different mortgage lenders.

What are the closing costs?

Closing costs include items like appraisal fees, title insurance fees, attorney fees, pre-paid interest and documentation fees. These items are usually different for each customer due to differences in the type of mortgage, the property location and other factors. You will receive a good faith estimate of your closing costs in advance of your closing date for your review.

Which amounts are included in my monthly payments?

If you have a fully amortizing mortgage, portions of your monthly mortgage payment go toward loan principal and interest. If your mortgage carries mortgage insurance, a portion of your monthly mortgage payment will pay this also, unless the lender has paid your mortgage insurance or you have paid your mortgage insurance upfront. If you have set up an escrow account for your mortgage, then portions also go toward your property taxes and homeowners insurance.

What is PMI?

Private Mortgage Insurance is provided by a private mortgage insurance company to protect lenders against loss if a borrower defaults. Private Mortgage Insurance is generally required for a loan with an initial loan to value (LTV) percentage in excess of 80%. In most cases, this will mean that you will have to pay Private Mortgage Insurance if your down payment is less than 20% of the value of the home you are purchasing or refinancing. The cost of the mortgage insurance is typically added to the monthly mortgage payment.

What will my rate be?

Rates are based on a variety of factors such as the loan purpose, your credit history and ability to repay, the value of the collateral and the loan amount.

What is an FHA mortgage?

FHA loans are government-insured loans through the U.S. Department of Housing and Urban Development, also called HUD. FHA loans offer an excellent start to first-time home buyers, with options such as a low down payment or a low closing cost option.

Quick Facts:

· Low down payment is required

· Your own personal savings are not required to pay down payment or closing costs. Gift funds may be used instead

· FHA may allow as low as 3.5% down payment down to a 580 score and 10% down payment to a 500 score.

How does my escrow account work?

An escrow account is a separate account that holds funds for the purpose of paying bills such as homeowner's insurance and property taxes. The lender collects the funds to be deposited into the account each month along with your monthly payment and then pays the bills for you when they come due. By taking the annual amounts charged for homeowner's insurance, property taxes and other annually paid items and dividing them by 12, a payment amount is determined and is added to your monthly principal and interest payment. Spreading the cost of these expenses over 12 months makes it easier for you to budget those expenses and you won't have to come up with additional cash when bills are due. For some loans, escrow accounts are a requirement.

What are the advantages of a home purchase?

A home purchase gives you personal benefits such as a sense of investing in your community and pride for achieving the dream of homeownership. There are some strong financial benefits as well, especially the tax savings you may enjoy. Interest payments on a mortgage are typically tax deductible (consult your tax advisor for more information). As you continue to make mortgage payments, you'll build home equity, as opposed to paying rent to someone else.

How much do I need for a down payment?

There is no set amount. In fact, you might be surprised to learn that many first-time homebuyer programs require as little as 3% down and potentially less on MN Housing or USDA Rural Development income based programs. Today, there are many loan programs that can be tailored to fit your needs and financial resources. Keep in mind that for down payments of less than 20% on conventional loans, private mortgage insurance (PMI) will be required.

Which is better: a fixed or adjustable interest rate?

If you plan to be in your home for more than seven years, you may want to consider a fixed-rate mortgage, which offers predictable payments and long-term protection against rising mortgage interest rates. If you plan to be in your home for seven years or less, an adjustable-rate mortgage (ARM) could be attractive. Keep in mind that with an ARM, your monthly payments have the potential to go up each time your interest rate adjusts.

Can I buy a home if I have less-than-perfect credit?

Yes. Keep in mind that lenders don't just look at your credit history, but also at your ability and willingness to pay in the future. Also at Eagle Home Mortgage we have a Home Buyer’s Solutions Group that can review your current credit profile and put together a plan of action that may assist you in improving your credit score and/or rating.